Unsupervised Anomaly Detection in Brain MRI

Comparison Analysis between 3D AutoEncoder vs 3D Denoising Diffusion Probabilistic Model

Sora Owada

on 2026-03-22

with

No Comments

Unsupervised Anomaly Detection in Brain MRI

Comparison Analysis between 3D AutoEncoder vs 3D Denoising Diffusion Probabilistic Model

My name is Kenny Shema, and I am a class of 2025 student pursuing a major in Computer Science and Economics.

My project consists of a personalized music recommendation system that uses real-time heartbeat data to suggest songs matching the user’s current mood or energy level. Built with a focus on integrating wearable sensor data and machine learning, the project aims to enhance emotional connection and user experience through adaptive, data-driven music selection.

My name is Helena Aleluya José, and I’m an international student from Angola. I’m also a Computer Science and Theater double major, and an African and African-American Studies and Creative Writing double minor. As both a computer scientist and a playwright, I wanted to create a project that reflects the intersection of my passions. For my senior capstone, I developed a framework that applies topic modeling techniques (LDA) to a corpus of dramatic texts in order to study playwright originality

This capstone project aims to develop a novel approach for analyzing and comparing playwrights’ unique voices and styles by applying topic modeling techniques, specifically Latent Dirichlet Allocation (LDA), on a corpus of theater texts. By leveraging advanced natural language processing (NLP) methods, the project will preprocess and prepare a diverse collection of plays for topic modeling, implement custom algorithms tailored for dramatic literature, and analyze the discovered topics to identify recurring themes, character archetypes, and narrative structures prevalent across different playwrights’ works. Interactive visualization tools will be developed to facilitate the exploration and interpretation of these insights, enabling literary scholars and critics to understand the creative processes better and the influences that shape dramatists’ voices.

Keywords

Topic modeling techniques, textual analysis, LDA model, Digital Humanities

Pet identification is important for veterinary care, pet ownership,

and animal welfare and control. This proposal presents a solution

for identifying dog breeds using dog images. The proposed method

applies a deep learning approach to identify the dog breeds. The

starting point for this method is transfer learning by retraining

existing pre-trained convolutional neural networks on the Stanford

Dog database. Three classification architectures will be used. These

classifiers will take images as input and generate feature matrices

based on their architecture. The stages these classifiers will undergo

to create feature vectors are 1) Convolution to generate feature

maps and 2) Max Pooling: highlight features are extracted from

the feature maps. Data augmentation is applied to the database to

improve classification performance.

The new version is the one used for the project but ver 5 was the last version to still include the sources for pitch A.

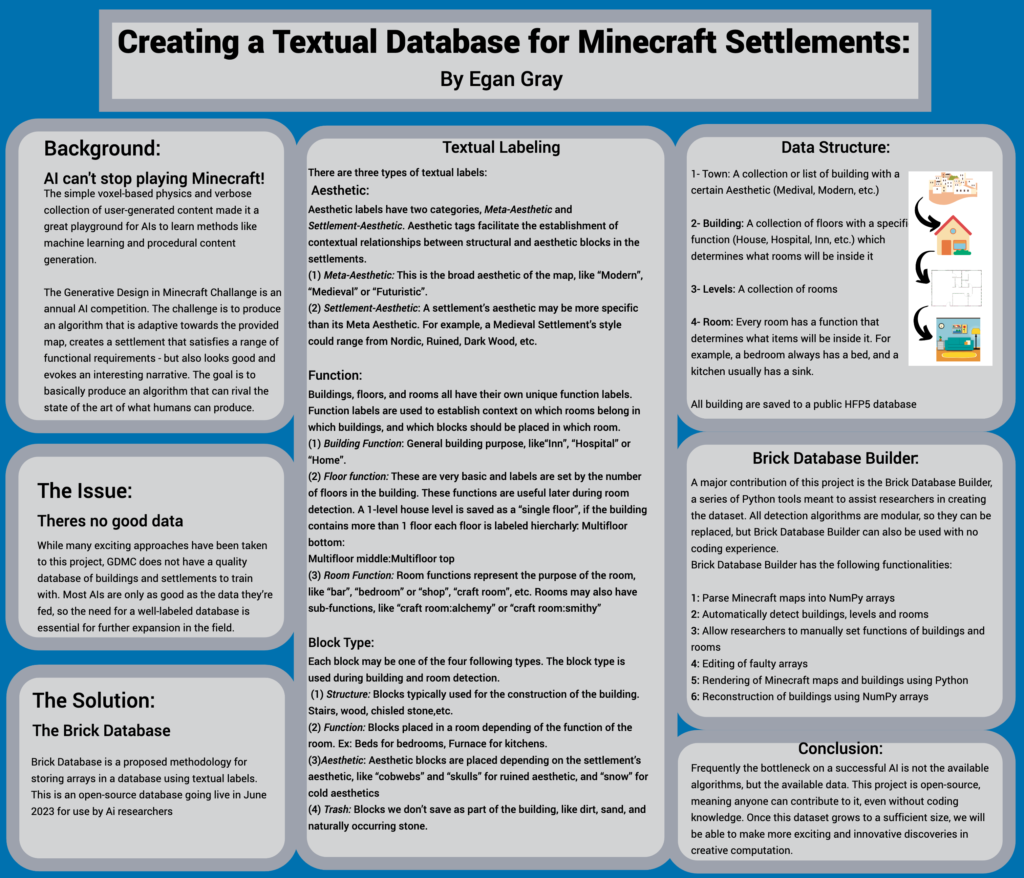

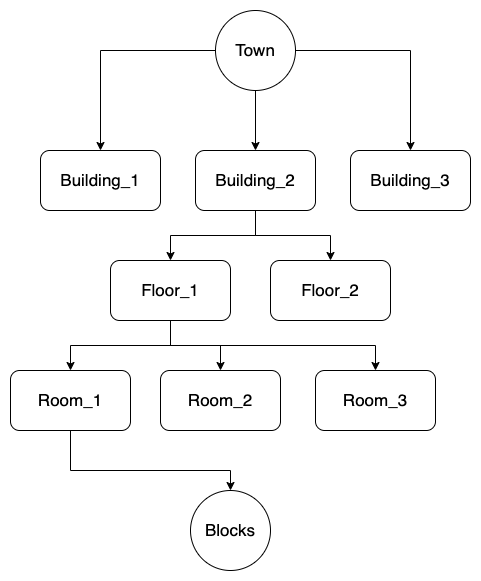

Abstract:

This paper presents the structure and design of a novel open-source textual database named the Brick Database for Minecraft settlements. Aimed at addressing the current lack of comprehensive datasets for model training in the Generative Design in Minecraft Competition (GDMC), this study explores the methodologies and potential challenges in creating a textual database and automatically detecting buildings and rooms.

Paper:

Software demonstration:

Poster:

Data diagram:

This project aims to build a system that uses machine learning algorithms to generate original music compositions based on original ones. This project will be studying machine learning techniques for pattern recognition.

The feedback I received from this seems to be more approachable than my first pitch, but I haven’t been able to receive more feedback because nobody has experience with this matter.

However, Doug questioned if there are Machine learning packages that I could use to build my project. Because in my project I aim to produce a new product from already existing ones. So, do we have packages to generate a new thing? It is possible to configure a train to produce something new.

I am currently getting in contact with the music department because there is a professor who teaches a class, “Making Music with Computer.”

I learned about software for music composition called “Max” which is a visual programming language for music and multimedia. I also learn about authors as David Cope, who he has a lot of work regarding artificial intelligence in music. I also investigated different types of music algorithms for composition and am currently looking for a specific problem or field to explore in this area.

Figure out because off all the complexity of this keep things simple.

Nowadays, it is very easy to get access to a lot of content online, including music, articles, games, videos, and movies. In the last couple of years, the use of video platforms such as YouTube has become very important for education, entertainment, hobbies, etc. However, YouTube is a platform where anyone can upload content, and not all content is appropriate to everyone. It can be because they may include sensitive content or bad words. This project will aim to use deep learning and machine learning for video analysis. It will require image processing to process video clips. It can also work with pattern recognition. This project aims to detect images and audio from the videos.

Challenge: video processing,

Data set of video file tag if they are not appropriate for children.

Potential dataset:

https://zenodo.org/record/3632781 (Restricted)

https://figshare.com/articles/dataset/The_Image_and_video_dataset_for_adult_content_detection_in_image_and_video/14495367/1 (adult content detention)

Youtube Data API (meta data)

Good Resources

This project aims to use machine learning to accurately translate real-time sign language to text by capturing sign language gestures using a camera (more likely from a computer’s web camera) to text. This system should be able to recognize various signs. I would like to study computer vision techniques.

From the input I received from Doug, this is a very ambitious project. We thought about what would be more convenient. Translate from moves gestures to text or from text to moves gestures. The first option seems to be more complicated because computer vision techniques can be a vast area. More than understanding computer vision techniques, but will also be required to recognize sign language and the context. To be able to train machine learning, I will require a lot of data that may not be easy to obtain.

This project will aim to have a friendly user interface. So it will be easy for the user to navigate through the translator.

Stroke is a cerebrovascular disease and is a significant causes of death. It causes significant health and financial burdens for the individual and the system. There are many machine-learning models built to predict the risk of stroke or to automatically diagnose stroke using predictors such as life factors or images. However, there has not been an algorithm that can predict using lab tests.

Idea #1

My research question:

What algorithms can be used to simulate policy making?

Public policy should obviously be for all citizens, but people often feel that their voices and real needs are not reflected in policy. In my home country of Japan, I have witnessed many voices on Twitter (now called X) about the policies they want from the government. I would like to create software that can use government data to simulate and predict what the impact would be if the government actually implemented those policies. Such a tool would help in better evidence-based policy making.

Idea #2

My research question:

How can we combine speech recognition, AI, and data extraction to automatically and instantly display the data mentioned in public discussions?

In Japan, when public policies are made, they have to be discussed in the Council or the Diet (Japanese national congress) in order to be approved. However, these discussions are often not easy to understand for the citizens for the following two reasons.

If the data (graphs and numbers) are automatically displayed when politicians refer to data by recognising the voice, policy-making will be more evidence-based and discussions will be easier for citizens to understand.

Idea #3 Computational Modeling of National Budget

My research question:

What algorithms can be used to better allocate the national budget?

What I realized while working with the government agencies in Japan last summer was that the policy-making process focuses heavily on the rationale of policies, and after they are approved, the evaluation is not as important as it should be. This could lead to a situation where the national budget continues to be allocated to policies that are not effective. If we can create a system to quantify the impact of each policy and also get comments from citizens, and use an algorithm to allocate the national budget, I think we could have a better cycle of public policy.

Facial Expression Recognition: This pitch will focus on facial expression recognition (FER) using convolutional neural networks (CNNs), which helps people with difficulties in communication, analyzes human’s emotion, and helps with development of AI in supporting humans during their daily life. Dataset: CK+ : 48×48 pixels images in grayscale format; face cropped; emotions includes anger (45 samples), disgust (59 samples), fear (25 samples), happiness (69 samples), sadness (28 samples), surprise (83 samples), neutral (593 samples), contempt (18 samples). Tufts Face Database: multi-modal face image images with more than 100,000 images, 74 females and 38 males from different age groups.

Kai Wang, Xiaojiang Peng, Jianfei Yang, Shijian Lu, and Yu Qiao. 2020. Suppressing uncertainties for large-scale facial expression recognition. Proceedings of the IEEE/CVF conference on computer vision and pattern recognition (2020), 6897–6906. https://openaccess.thecvf.com/content_CVPR_2020/html/Wang_Suppressing_Uncertainties_for_Large-Scale_Facial_Expression_Recognition_CVPR_2020_paper.html

This paper addressed a specific problem in large-scale FER, which is “uncertainties caused by ambiguous facial expression, low-quality facial images, and the subjective of the annotators” by using the Self-Cure Network. Because it focuses on a problem in FER, it is a good example if we want the purpose of our proposal to be about addressing a problem in the domain. It also mentions a lot of good dataset for FER along with works on FER using algorithms in the citation, which are good resources for our proposal. Related works in the field are also provided and went into detail to showcase the problem that the paper is focusing on. The methods that were proposed in the paper are based on the observation that CNNs can be uncertain about their predictions.

Shervin Minaee, Mehdi Minaei, and Amirali Abdolrashidi. 2021.Deep-Emotion: Facial Expression Recognition Using Attentional Convolutional Network. Sensors 21, 9, 3046. https://www.mdpi.com/1424-8220/21/9/3046

This paper is about FER using attentional CNNs. It discusses the challenges of FER and how attentional CNNs can be used to address them. The author proposed a new attentional CNN architecture that is able to focus on important facial regions for emotion detection. Because I decided to use CNN as the main method for processing the data in my paper, I can consider using the proposed attention CNNs from this paper. The proposed attentional CNN architecture consists of 2 main components: a feature extraction network and an attention network. The feature extraction network extracts features from the input image, while the attention network learns to focus on the most important facial regions for emotion detection.

Yunxin Huang, Fei Chen, Shaohe Lv, and Xiaodong Wang. 2019. Facial expression recognition: A survey. Symmetry 11, 10, 1189. MDPI. https://www.mdpi.com/2073-8994/11/10/1189

This paper is a survey for FER of visible facial expressions, which provides a lot of necessary background knowledge like terminologies and difficulties in the field. It also provided a throughout FER approach from beginning to end process including Image processing, feature extraction, gabor feature extraction, and expression classification. CNNs, Deep Belief Network, Long Short-Term Memory, Generative Adversarial Network are introduced and cited with current works related to them.

M. A. H. Akhand, Shuvendu Roy, Nazmul Siddique, Md Abdus Samad Kamal, Testuya Shimamura. 2021. Facial emotion recognition using transfer learning in the deep CNN. Electronics 10, 9, 1036. MDPI. https://www.mdpi.com/2079-9292/10/9/1036

This paper focuses on Deep CNN and Transfer Learning (TL). CNN is a popular technique used for FER and it is one that I’m considering moving forward with. This paper also focuses on using these techniques to reduce the development efforts, which is an understanding problem that all of the previous ones haven’t touched on. FER systems need to be able to handle occlusion, noise, and other challenges. Deep CNNs have been shown to be effective for FER tasks. CNNs are able to learn complex features from images, which can be helpful for identifying FER. Transfer learning is a technique where a pre-trained model is used as a starting point for a new model. This can be useful for tasks where there is limited training data available. In the paper, they introduced the technique of adopting a pre-trained Deep CNN model and replacing its dense upper layer(s) compatible with FER, and then fine-tuning the model with facial emotional data. This approach has been shown to achieve remarkable accuracy on both the FDEF and JAFFE facial image datasets.

Roberto Pecoraro, Valerio Basile, and Viviana Bono. 2022. Local multi-head channel self-attention for facial expression recognition. Information 13, 9, 419. MDPI. https://www.mdpi.com/2078-2489/13/9/419

This paper proposed Local multi-head Channel self-attention (LHC) in the context of computer vision and in facial expression recognition. LHC is a very new approach in the field of FER. This paper will be useful because the LHC module is a type of self-attention module that can be integrated into CNNs, and it has been shown to improve the performance of CNNs on FER tasks. In a CNN, each layer learns to extract different features from the input image. The LHC module allows the CNN to learn long-range dependencies between features, which can be helpful for FER.

Peter Anderson, Basura Fernando, Mark Johnson, and Stephen Gould. 2016. Guided open vocabulary image captioning with constrained beam search. arXiv preprint arXiv:1612.00576. https://arxiv.org/abs/1612.00576

I read this paper for another class, and I think it is pretty interesting if I can incorporate this into my paper. The paper proposed a method for improving the performance of open vocabulary image captioning models. Open vocabulary image captioning models are able to generate captions that contain words that are not present in the training data. The author introduced a technique called constrained beam search to guide the generation of captions. Contrainsed beam search forces the generated captions to include certain words. FER uses words “happy”, “sad”, “angry”, and “neutral”, constrained beam search could be used to force the system to predict at least one of these words in each prediction.

Sentiment analysis of online food reviewWhen people buy products online, the one thing that they tend to look closely at are the reviews of the product. Having good reviews and understanding the needs of the customers through the review can help the business grow tremendously. A review usually comes in two parts: the rating and the reviews. While the text-review system can be easy to interpret the customers’ overall experiences without any biases, the star-rating system tends to be less informative and it is up to the viewer to interpret the rating. This project aims to perform sentiment analysis on the reviews dataset, so it provides more accurate feedback on the products. Another aspect that this project can develop toward is that it can perform analysis on the negative languages on the recent reviews to let the businesses know what they should focus on improving. Amazon Fine Food Reviews dataset, which contains data over a 10 year period (1999 to 2012). Another plan to replace this dataset is using DoorDashAPI to collect reviews from the restaurants on DoorDash.

Yi Luo, and Xiaowei Xu. 2021. Comparative study of deep learning models for analyzing online restaurant reviews in the era of the COVID-19 pandemic. International Journal of Hospitality Management 94, 102849. Elsevier. https://www.sciencedirect.com/science/article/pii/S0278431920304011

The paper performs analysis on four features of 112,412 restaurants on Yelp and shows outcome comparison between algorithms. The data are collected by using a web scraper, which is a method that we proposed for our paper if we can’t find a more recent dataset. They also mentioned the process of data cleaning, which includes 2 procedures: tokenization and stopwords removal. They provided 2 deep learning and machine learning algorithms: gradient boosting decision tree classifier, random forest classifier, bidirectional LSTM, and simple word-embedding model. They also proposed both theoretical and practical implications for future work, which is a good place to find motivation for our paper.

Mayur Wankhade, Annavarapu Chandra Sekhara Rao, and Chaitanya Kulkarni. 2022. A survey on sentiment analysis methods, applications, and challenges. Artificial Intelligence Review 55, 7, 5731-5780. https://link.springer.com/article/10.1007/s10462-022-10144-1

This paper provided a background on sentiment analysis like the survey for FER, which also gives us a good start to understanding how to approach sentiment analysis. It provides a throughout beginning-to-end process of a sentiment analysis. I find it useful when reading about the 3 main approaches, which are Lexicon Based Approach, Machine Learning Approach, and Hybrid Approach. It also introduced some common machine learning algorithms for sentiment analysis: Naive Bayes, support vector machines, and deep learning. Naive Bayes is easy to implement and can be trained on a relatively small dataset. Support vector machines can be trained to achieve high accuracy, but they can be more difficult to implement and require a larger dataset than Naive Bayes. Deep learning algorithms like recurrent neural networks and CNNs are more difficult to implement and require a large dataset to train.

M. Govindarajan. 2014. Sentiment analysis of restaurant reviews using hybrid classification method. Sentiment analysis of restaurant reviews using hybrid classification method 2, 1, 17-23. https://www.digitalxplore.org/up_proc/pdf/46-1393322636127-133.pdf

This paper compared the effectiveness of different methods made for classifying restaurant reviews and whether it is beneficial to use ensemble techniques. It includes methods like Naive Bayes, Support Vector Machine and Genetic Algorithm. I think they provide a broad look at what methods are available for classification and that can be helpful for our paper, but I am not sure if it will be useful for our paper since we are not planning to explore classification in restaurant reviews but more about the sentimental analysis of it. However, the amount of paper available on the topic that I proposed is quite limited. If we can get access to one of the paper I listed below, they can be a good resource since it is more related to the direction I want to develop my proposal.

Anirban Adak, Biswajeet Pradhan, and Nagesh Shukla. 2022. Sentiment analysis of customer reviews of food delivery services using deep learning and explainable artificial intelligence: Systematic review. Foods 11, 10, 1500. MDPI. https://www.mdpi.com/2304-8158/11/10/1500

This paper focuses on AI and DL for sentiment analysis. They explained more about how AI, DL, ML are developing within each other. I think this paper acts as an overall guide on the techniques that I should use for my paper. It includes information about different AI methods that are used in sentiment analysis of customer reviews for food delivery services and also challenges when using DL techniques on customer reviews.

Maria Kostromitina, Daniel Keller, Muhittin Cavusoglu, and Kyle Beloin. 2021. “His lack of a mask ruined everything.” Restaurant customer satisfaction during the COVID-19 outbreak: An analysis of Yelp review texts and star-ratings. International journal of hospitality management 98, 103048. Elsevier. https://www.sciencedirect.com/science/article/pii/S0278431921001912

This paper is similar to what I might want to do for my pitch: it includes background information about the review text in relation to the choice of star-ratings. It also provides an interesting aspect of how Covid-19 affected the reviews of the customers, and how, depending on the situations, the reviews that the customers read might not help them make the right decision of choosing a good restaurant.

Ruba Obiedat, Raneem Qaddoura, Al-Zoubi Ala’M, Laila Al-Qaisi, Osama Harfoushi, Mo’ath Alrefai, and Hossam Faris. 2022. Sentiment analysis of customers’ reviews using a hybrid evolutionary svm-based approach in an imbalanced data distribution. IEEE Access 10, 22260–22273. IEEE. https://ieeexplore.ieee.org/abstract/document/9706209/

This paper, other than proposing new techniques for sentiment analysis, addresses the problem of imbalance dataset, which is a common problem to encounter in data analysis. Even thought, the paper doesn’t perform the work on an English-based dataset, it is useful to see how they deal with imbalance data problems. They use Naive Bayes, SVM, and Genetic Algorithm on the dataset, then compare with their proposed hybrid model built with all three classification methods

Pitch 1: Reduce the encounter of local minima in heuristic search space. In the heuristic search space of heuristic algorithms, there are areas where the nodes appear to be closer to the goal state, but when the algorithm encounters these areas, they actually wasted more resources to reach the goal. These areas are called local minima. Local minima tends to arise more when using distance to go as the heuristic value instead of cost to go, which is an aspect that this project plans to explore. Avoiding local minima and understanding the behavior can help improve the performance of heuristic search algorithms. Overall, this project will explore the problem of local minima with beam search.

Risk: There is limited information on this topic and a lot of knowledge gaps that will need to be filled.

Pitch 2: Facial expression recognition: classify facial expression using machine learning. Problem: help people in communication, analyze human’s emotion, help with the development of AI in supporting humans during their daily life. Dataset: CK+ : 48×48 pixels images in grayscale format; face cropped; emotions includes anger (45 samples), disgust (59 samples), fear (25 samples), happiness (69 samples), sadness (28 samples), surprise (83 samples), neutral (593 samples), contempt (18 samples). Tufts Face Database: multi-modal face image images with more than 100,000 images, 74 females and 38 males from different age groups.

Risk: Finding a suitable machine learning algorithm, process image data.

Pitch 3: Sentiment analysis of online food review. When people buy products online, the one thing that they tend to look closely at are the reviews of the product. Having good reviews and understanding the needs of the customers through the review can help the business grow tremendously. A review usually comes in two parts: the rating and the reviews. Users, a lot of the time, mistakenly choose the wrong rating for the products, so the reviews are more reliable in most situations. This project aims to perform sentiment analysis on the reviews dataset, so it provides more accurate feedback on the products. Another aspect that this project can develop toward is that it can perform analysis on the negative languages on the recent reviews to let the businesses know what they should focus on improving. Amazon Fine Food Reviews dataset, which contains data over a 10 year period (1999 to 2012). Another plan to replace this dataset is using DoorDashAPI to collect reviews from the restaurants on DoorDash.

Risk: dataset is not recent and will keep looking for a more recent dataset.

In today’s digital world, where online content is easily accessible, my project aims to use deep learning and machine learning techniques, such as Neural Networks, to tackle the challenge of inappropriate content on video platforms like YouTube. Using advanced image processing and pattern recognition, my goal is to detect and flag unsuitable imagery and audio within videos. With a focus on creating a child-safe environment, I aim to build a comprehensive dataset of video file tags, making online platforms more secure for users of all ages and fostering a responsible and enjoyable digital experience.

Research question: To improve the accuracy and efficiency of content classification on YouTube, can I compare and evaluate the performance of different deep learning architectures, such as Convolutional Neural Networks (CNNs) and Recurrent Neural Networks (RNNs) versus human judgment, in the context of detecting inappropriate content? What are the trade-offs in terms of computational resources and real-time processing?

Datasets:

https://zenodo.org/record/3632781 (Restricted)

https://figshare.com/articles/dataset/The_Image_and_video_dataset_for_adult_content_detection_in_image_and_video/14495367/1 (adult content detention)

YouTube Data API (metadata)

Good Resources:

2. Pitch #2: Machine learning for music recognition:

This project aims to use machine learning for music genre recognition. In a world where music is everywhere, music recognition can be a bit of a challenge. I will use machine learning techniques to teach the system to recognize unique patterns and characteristic that defines the music genre. I may try to duplicate already well-known models for music recognition and compare two of them to see which one is more efficient.

Research question: To optimize music genre recognition using machine learning, can we compare and evaluate the performance of traditional machine learning classifiers, such as logistic regression and support vector machines (SVMs), with deep learning architectures like convolutional neural networks (CNNs) using a diverse dataset? How do these algorithms perform in terms of accuracy?

Data sets:

Saki Pitches

This is a test

This is a test

About Me:

I am Andex Nguyen, a Senior who’s majoring in Data Science.

Introduction:

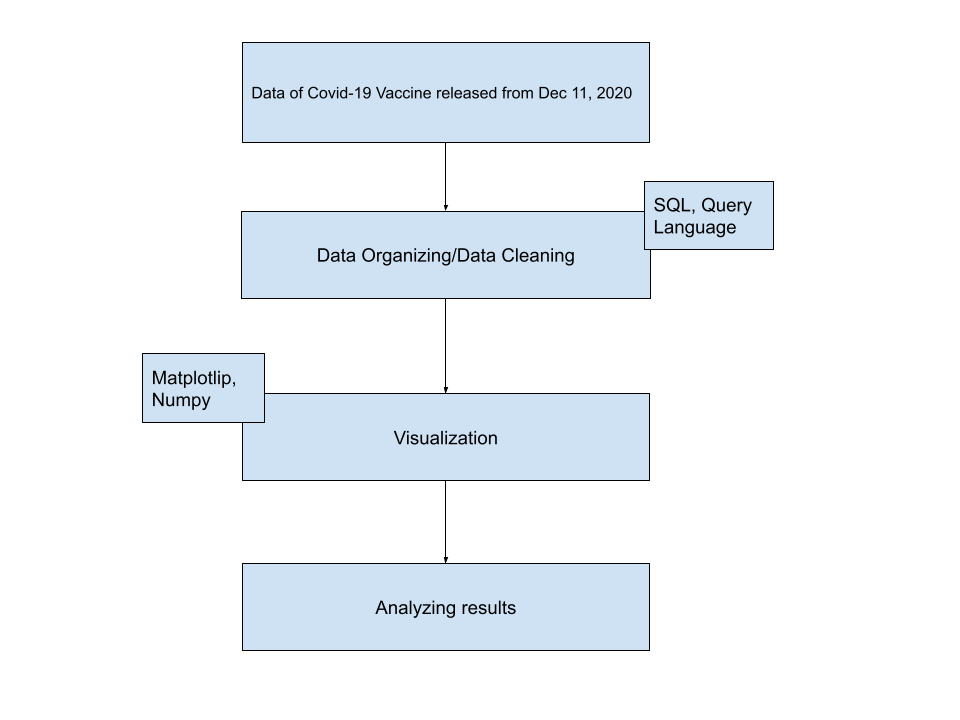

Since 2020 when the pandemic struck us for the first time, Covid-19 has always been a globally noteworthy issue. In this project, the questions that I am trying to find the answers for are how different countries in 1 region, specifically South-East Asian Countries, responded to the Vaccine, and what may be the reasons for that difference. A lot of the time, the matter of the people not having vaccinated stem from the political issues, economic and medical ability to acquire the vaccines, and the belief systems of those countries. My country, Vietnam, did very well in preventing Covid-19 by executing strong quarantine policies for our first step, and we proceeded to excellently secure an adequate amount of vaccines for our people. I want to see if the countries around the same area as my country also did a similarly good job. There would also be a case difference between fully vaccinated and those who are still waiting to complete their vaccination process.

Data Architecture Diagram:

GitLab link:

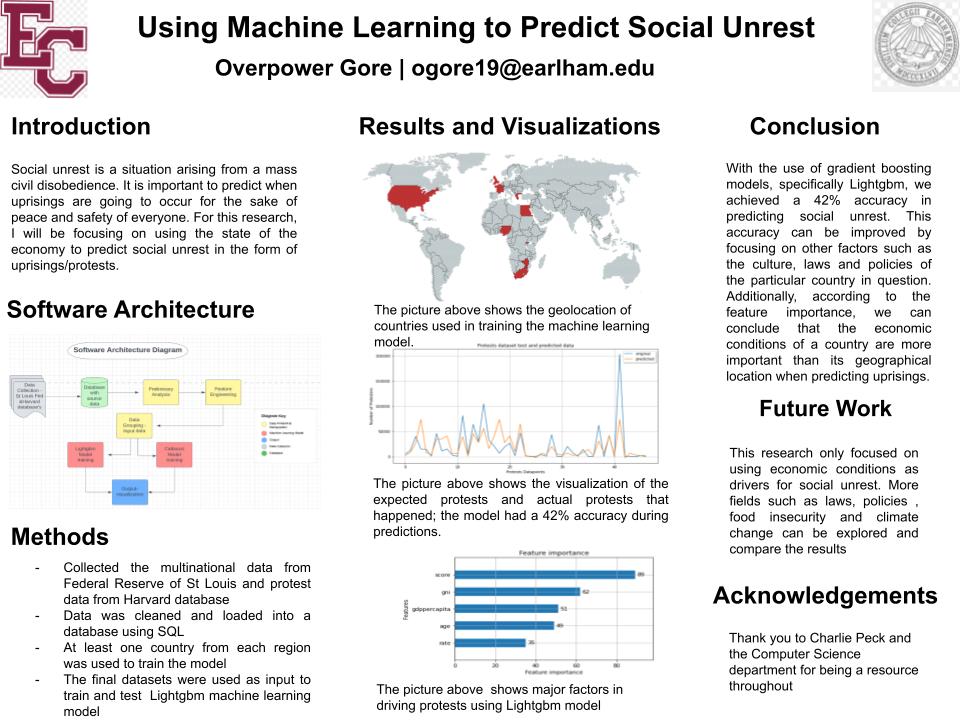

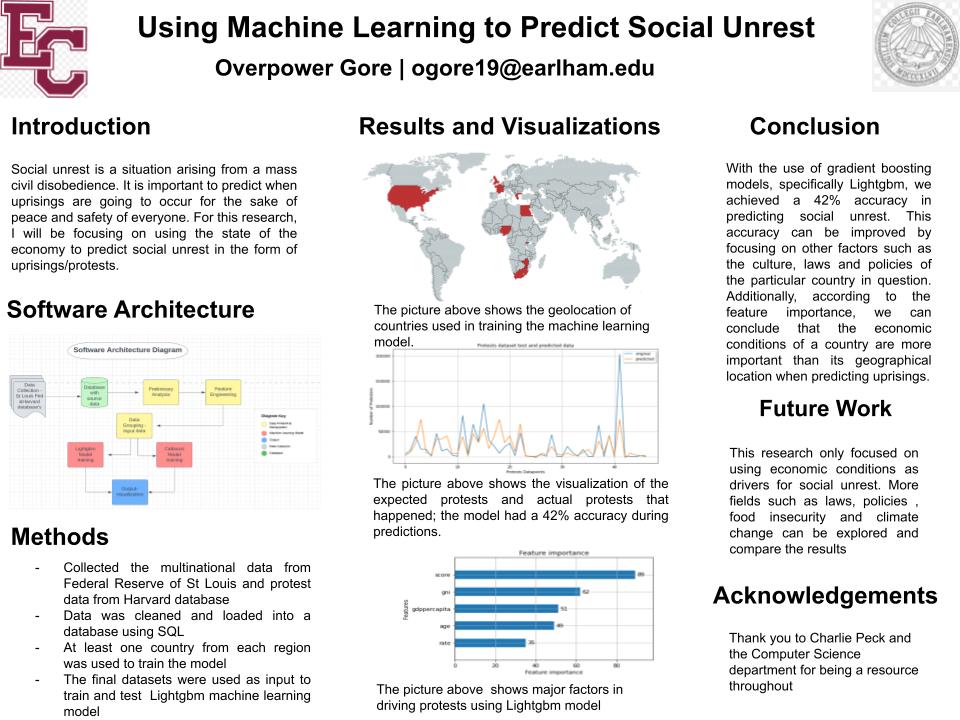

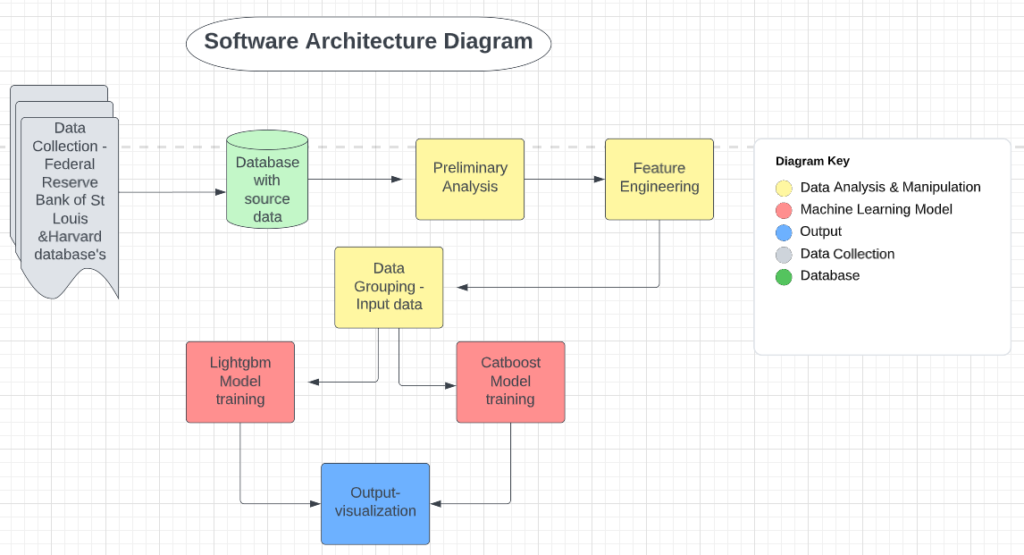

Uprisings are an act of resistance/rebellion. Uprisings could be the general population rising against the government (such as the protests in Zimbabwe as people protest over the poor economic conditions) or it could be people with morally questionable intentions against the general populace such as the Boko Haram in Nigeria. It is important to predict when uprisings are going to occur for the sake of peace and safety of everyone. This leads to the question of how we can possibly know before a social upheaval begins. Currently there is no official way to predict social unrest or a protest; people only know when a protest has already started. For this research, I will focus on using machine learning to study the effects of economic trends causing social uprisings. I use the trained machine learning model to predict when social upheaval’s are likely to happen. This model will be continually improved by doing exploratory data analysis to see which financial metrics are more reflective of the economy at any given time and using those metrics as input into the model. Continuously improving the accuracy of the model means we get closer to accurately predicting social unrest consequently ensuring the peace and safety of the public in the event of a protest

Hi, my name is Overpower Gore but everyone calls me OPG. I am a senior Data Science student at Earlham College with a passion for information technology. I have held multiple internships impacting positive organizational outcomes through software development, data analysis, and data visualization.

1)

I am interested in completing research related to the use of machine learning to generate decision trees which control non-player character behavior in video games. Decision trees are relatively interpretable and have a high-level correspondence to behavior trees, which are used in the most common approach to AI for video games (Świechowski, 2022). I also enjoyed working with them when I took Artificial Intelligence and Machine Learning. The two environments I would propose using for testing is the Micro-Game Karting template in the Unity Asset Store, which is available for free and was used for testing by Mas’udi (2021).

Annotated Bibliography

Chan, M. T., Chan, C. W., & Gelowitz, C. (2015). Development of a Car Racing Simulator Game Using Artificial Intelligence Techniques. International Journal of Computer Games Technology, 2015.

This paper argues that Unity, as a development platform for a racing game, has advantages over the use of traditional AI search techniques for implementation of path-finding. These points could help to justify a decision to utilize Unity as an environment for testing.

Fairclough, C., Fagan, M., Mac Namee, B., & Cunningham, P. (2001). Research Directions for AI in Computer Games. Department of Computer Science, Trinity College, Dublin.

This article gives a number of reasons for the simplicity of AI used by game developers in comparison to that used in academic research and industrial applications, and mentions a number of well-understood techniques in wide use at the time of its publication, including FSMs and A*. It also offers a number of reasons why research into AI for computer games is a worthwhile endeavor.

French, K., Wu, S., Pan, T., Zhou, Z., & Jenkins, O. C. (2019, May). Learning Behavior Trees from Demonstration. In 2019 International Conference on Robotics and Automation (ICRA) (pp. 7791-7797). IEEE.

This article gives advantages of behavior trees and describes two methods by which a decision tree can be converted to a behavior tree. This could be helpful in understanding the relationship between the decision trees which I intend to work with and the behavior trees that are prevalent in video game AI.

Guo, X., Singh, S., Lee, H., Lewis, R. L., & Wang, X. (2014). Deep Learning for Real-Time Atari Game Play Using Offline Monte-Carlo Tree Search Planning. Advances in Neural Information Processing Systems, 27.

This paper presents results from game-playing agents whose performance was tested on the ALE, an environment which includes a variety of games for the Atari 2600 and thus would allow for testing the performance of decision trees on a range of different games, as well as permitting straightforward evaluation of the agent’s performance through scores achieved on the seven games used to evaluate Deep Q-Network. It also offers an example of the use of a method that would be infeasible for real-time play to generate training data for a faster agent, which, similar to the use of machine learning to generate a decision tree, uses a time-intensive process to create a classifier which can make decisions in real time.

Mas’udi, N. A., Jonemaro, E. M. A., Akbar, M. A., & Afirianto, T. (2021). Development of Non-Player Character for 3D Kart Racing Game Using Decision Tree. Fountain of Informatics Journal, 6(2), 51-60.

This article offers an example of the use of decision trees to control NPC behavior. The environment it uses, Micro-Game Karting, which is now known as Karting Microgame, also offers an accessible environment for testing the performance of decision trees.

Van Lent, M., Fisher, W., & Mancuso, M. (2004, July). An Explainable Artificial Intelligence System for Small-Unit Tactical Behavior. In Proceedings of the national conference on artificial intelligence (pp. 900-907). Menlo Park, CA; Cambridge, MA; London; AAAI Press; MIT Press; 1999.

This paper offers an example of one approach to transparency of video game AI, that of creating a distinct system to explain its action in retrospect, as well as a different context in which explainability is relevant. It could be compared with the use of behavior trees and decision trees to allow for transparency in video games.

2)

I wish to complete research related to the use of databases in video games to improve the efficiency of computations by increasing data locality and taking advantage of the optimizations of database management systems. While the article and dissertation by O’Grady (2019, 2021) which are referenced below both appear to focus on the feasibility of that approach, it seems likely that additional exploration is warranted regarding demonstrable advantages. For this exploration, I would propose focusing on the execution of path-finding through a database management system, one of the main areas examined by O’Grady (2021). Specifically, I wish to focus on sub-optimal path-finding, since optimality is generally not essential in the context of video games (Botea, 2013), despite the widespread use of A* (Kapi, 2020).

Annotated Bibliography

Abd Algfoor, Z., Sunar, M. S., & Kolivand, H. (2015). A Comprehensive Study on Pathfinding Techniques for Robotics and Video Games. International Journal of Computer Games Technology, 2015.

This article offers an overview of the various pathfinding techniques used for video games and robotics. It is organized by environment representation and could be helpful in comparing and evaluating path-finding algorithms in order to determine which to use with a specific representation. It might also assist in deciding on an environment representation.

Bendre, M., Sun, B., Zhang, D., Zhou, X., Chang, K. C., & Parameswaran, A. (2015, August). Dataspread: Unifying databases and spreadsheets. In Proceedings of the VLDB Endowment International Conference on Very Large Data Bases (Vol. 8, No. 12, p. 2000). NIH Public Access.

This paper describes a system created by unifying relational databases and spreadsheets, with the goal of retaining the advantages of spreadsheets while taking advantage of the power, expressivity, and efficiency of relational databases. The objective and approach of this research bear significant resemblances to those of O’Grady’s 2021 dissertation, in that both seek to increase the efficiency of a system by handling costly computations in a relational database. However, this article differs from O’Grady’s work in that it is based on a spreadsheet interface and an underlying database, rather than focusing on the implementation of specific components of a system within a database management system.

Botea, A., Bouzy, B., Buro, M., Bauckhage, C., & Nau, D. (2013). Pathfinding in games. Schloss Dagstuhl-Leibniz-Zentrum fuer Informatik.

This paper explains the logic and advantages of various approaches to path-finding in video games. It also recognizes that in video game contexts, suboptimal paths are acceptable

O’Grady, D. (2019). Database-Supported Video Game Engines: Data-Driven Map Generation. BTW 2019.

This paper provides a demonstration of how a portion of a game’s internals can be moved to a database system. Its goal is to show that the benefits of moving expensive computations to a database system can be obtained while still allowing straightforward modification of the process by game developers.

O’Grady, D. (2021). Bringing Database Management Systems and Video Game Engines Together (Doctoral dissertation, Eberhard Karls Universität Tübingen).

This dissertation is the main work which I intend to build on in my thesis. Specifically, I wish to further explore the advantages of implementing path-finding in a database management system, as covered in Chapter 4.

Kapi, A. Y., Sunar, M. S., & Zamri, M. N. (2020). A review on informed search algorithms for video games pathfinding. International Journal, 9(3).

This paper provides an overview of various ways of optimizing informed search algorithms for path-finding in video games, presenting various factors which influence memory and time usage. It would be useful for considering potential consequences of different experiment designs, given its focus on approaches to improving the efficiency of path-finding which do not rely on the optimizations of a database management system.

1)

I am interested in completing research related to the use of machine learning to generate decision trees which control non-player character behavior in video games. Decision trees are relatively interpretable and have a high-level correspondence to behavior trees, which are used in the most common approach to AI for video games (Świechowski, 2022). I also enjoyed working with them when I took Artificial Intelligence and Machine Learning. The environment I would propose using for testing is the Micro-Game Karting template in the Unity Asset Store, which is available for free and was used for testing by Mas’udi (2021).

References

Chan, M. T., Chan, C. W., & Gelowitz, C. (2015). Development of a Car Racing Simulator Game Using Artificial Intelligence Techniques. International Journal of Computer Games Technology, 2015.

Guo, X., Singh, S., Lee, H., Lewis, R. L., & Wang, X. (2014). Deep Learning for Real-Time Atari Game Play Using Offline Monte-Carlo Tree Search Planning. Advances in Neural Information Processing Systems, 27.

Mas’udi, N. A., Jonemaro, E. M. A., Akbar, M. A., & Afirianto, T. (2021). Development of Non-Player Character for 3D Kart Racing Game Using Decision Tree. Fountain of Informatics Journal, 6(2), 51-60.

Świechowski, Maciej and Ślęzak, Dominik, Monte Carlo Tree Search as an Offline Training Data Generator for Decision-Tree Based Game Agents (2022). BDR-D-22-00241, Available at SSRN: https://ssrn.com/abstract=4152772 or http://dx.doi.org/10.2139/ssrn.4152772

2)

I am considering completing research related to the use of databases in video games for purposes apart from data storage. While the article and dissertation by O’Grady (2019, 2021) which are referenced below both appear to focus on the feasibility of that approach, it seems likely that additional exploration is warranted regarding demonstrable advantages. For this exploration, I would propose focusing on the execution of path-finding through a database management system, one of the main areas examined by O’Grady (2021).

References

Muhammad, Y. (2011). Evaluation and Implementation of Distributed NoSQL Database for MMO Gaming Environment (Dissertation, Uppsala University).

O’Grady, D. (2021). Bringing Database Management Systems and Video Game Engines Together (Doctoral dissertation, Eberhard Karls Universität Tübingen).

O’Grady, D. (2019). Database-Supported Video Game Engines: Data-Driven Map Generation. BTW 2019.

Jovanovic, R. (2013). Database Driven Multi-agent Behaviour Module (Thesis, York University).

3)

I am also considering completing research related to the use of machine learning for recognition of Kuzushiji, an old style of Japanese cursive writing. Kuzushiji mainly appear in works from the Edo period of Japanese history and are difficult to identify correctly due to their lack of standardization (Ueki, 2020). Another difficulty comes from the Chirashigaki writing style, in which text is not written in straight columns (Lamb, 2020). The Center for Open Data in the Humanities has released a dataset of them (Ueki, 2020), which is available at http://codh.rois.ac.jp/char-shape/.

References

Clanuwat, T., Bober-Irizar, M., Kitamoto, A., Lamb, A., Yamamoto, K., & Ha, D. (2018). Deep Learning for Classical Japanese Literature. arXiv preprint arXiv:1812.01718.

Clanuwat, T., Lamb, A., & Kitamoto, A. (2019). KuroNet: Pre-Modern Japanese Kuzushiji Character Recognition with Deep Learning. arXiv preprint arXiv:1910.09433.

Lamb, A., Clanuwat, T., & Kitamoto, A. (2020). KuroNet: Regularized Residual U-Nets for End-to-End Kuzushiji Character Recognition. SN Computer Science, 1(3), 1-15.

Ueki, K., & Kojima, T. (2020). Feasibility Study of Deep Learning Based Japanese Cursive Character Recognition. IIEEJ Transactions on Image Electronics and Visual Computing, 8(1), 10-16.

Machine Learning and Dueling:

A fighters skill comes from their training, their learned experience through failure, and thousands of reps. This is also exactly how reinforcement learning agents gain their skills– I propose a mutli-agent learning experiment where we attempt to teach two agents how to fight with swords and shields.

There are a couple common issues that hinder how AI’s learn in a 3D space. First, multi-agent learning (learning with two or more agents) is notoriously challenging. This is made difficult because an agent not only must learn how to move in general, but also move around another agent. As of 2017, a recent algorithm called MAD-DPG has proposed a solution to this problem, but it’s still buggy and could present issues. Additionally, without proper motion capture data, the agents will learn incorrectly, most commonly seen in issues like body parts artifacting through the ground. Finally, while I have motion capture data for individual fighting movements, such as slashing a sword or blocking with a shield, it is much more difficult to find motion capture data that of two humans sword fighting. Finally, swords and shields will be weighted, throwing off the model’s sense of balance, which will take lots of training to get used to.

Using Unity 3D machine learning agents made possible through PyTorch, CUDA and the unity facing engine, ML-agents, I propose I propose creating a deep reinforcement learning agent. Our control strategy would have 2 parts, a pretraining stage (a deep learning model used to create a neural network to solve problem) and a Transfer learning stage, which uses a prebuilt neural network from our pretraining stage to solve a problem.

Steps of pretraining:

Steps of Transfer Learning:

Social Simulation of Scaricity:

Scarcity–how do we divide resources fairly when their isn’t enough for everyone? The entire subject of Economics boils down to this question, and has caused many conflicts throughout history. Sometimes, we have to make tough decisions because of scarcity.

I propose an experiment in a simulated world, with two “tribes” of agents. The agents must eat once a day, which is done by collecting food blocks. Each agent has the ability to move, eat, collect food for their village, ask others to share, and kill eachother. Each agent’s main priority is to eat for as many days as possible. If they go a full day without eating, they starve to death.

Then, we test these tribes under different levels of scarcity:

If the agents have plenty, will they remain peaceful? If there’s a moderate distribution, will the tribes share with eachother and lose the same number of members? Will they fight the other tribes for resources? If the resources are scare, will a tribe sacrifice members of their own tribe, or steal from the other tribe? Is fighting inevitable with an unfair disruption?

In order to do this experiment, we must allow for a level of teamwork. Each tribe has their own Competive Learning Policy which builds a nueral network, judging its success by how many tribe members are left after a given period of days. These networks may give tasks such as move, attack or collect food to any tribe member.

Usually, two agents learning against eachother means slower learning, but because the neural network are essentially playing a simple strategy game against eachother, they’re learning might be accelerated due to the competition.

Creating Unique Architecture with Machine Learning:

Necessity, the mother of invention. From the water carrying aqueducts of Rome to the houses stacked across the mountains of Tibet, people have made unique and intricate structures out of necessity. Typically, neural networks are trained with data sets, which they then attempt to imitate according to a metric of success. However, what they produce isn’t truely unique, it’s an imitation of what a researcher asks them to create. I propose an experiment to create entirely unique, AI generated 3D architecture by providing the necessity to build.

First, we must make environment simple enough for an neural network to learn to create in, but succifciently complex enough to cultivate interesting innovation. Unity 3D is ideal to create this enviroment, as it already has a well-developed physics engine, adding additional enviromental conditions is simple, allows for easy map creation, has many free assets to use, and supports machine learning.

Second, we must create necessity. Two agents will be created, a Creature and a Creator agent. The Creature is a simple bot, who’s only goal is to keep his three needs satisfied. The creature wants to stay warm, dry, and well fed. Warmth is decreased when “wind” comes in contact with our agent, dryness is decreased when rain comes in contact with our agent, and hunger is decreased by collecting food blocks.

The Creator agent has a simple goal, keep the Creature as warm, fed, and dry as possible. The Creator is a neural network with the ability to build, under the conditions of the physics engine. This neural network has permission to use a limited amount of two different resources: Wood and stone. Stone is much stronger then wood, but also much heavier. Wood is weaker, so it breaks under weight, but also lighter and more accessible. Wood and stone come in blocks, and wood also comes in plank form, which is worse for walls but better for roofs. The Creator has the ability to “nail” materials together, which means the materials may be connected together through touching vectors, unless the weight of materials attached to it is too heavy to hold.

Beyond coming with a well developed and well tested physics engine, the beauty of the Unity engine is it’s ease of customimability. Because it’s a game engine, adding new conditions is made easy. Once our Creator network has learned to build basic structures, we can up the complexity of the structures by adding more needs. Possibilities include:

The goal is to create unique and interesting structures, and a simulation made too simple will lead to uninteresting building. Unity 3D’s easy ability to add and remove these conditions will be vital to this experiment, as these new conditions may create innovate, or break and confuse our neural network.

My name is Hang “Hailee” Dang. I am a senior majoring in Data Science with interest in Finance, Data and Business Analytics.

Hello! My name is Tamara and I am a senior Computer Science Major at Earlham College and this is my capstone project. I am interested in applying machine learning and other computational techniques for better understanding of social issues. Here is the abstract of my capstone project proposal.

Unmanned Aerial Vehicles (UAVs) have only recently been applied

in the detection of clandestine graves. With the growing technical

abilities of UAVs, more opportunities are available in methods

for recording data. This opened many doors for detecting hidden

graves because now many different sensing devices can be used

in remote areas that were inaccessible to humans. This study will

compare the use of hyperspectral and RGB images taken by drones

to detect hidden graves. It is aiming to compare how accurately

the graves can be detected post-image processing using the same

technique. The primary motivation is to help future researchers

more easily decide which data collection technique they should use.

The processing technique used on both data sets is a model with

an edge detection algorithm.

Hello! My name is Tamara and I am a senior Computer Science Major at Earlham College and this is my capstone project. I am interested in applying machine learning and other computational techniques for better understanding of social issues. Here is the abstract of my capstone project proposal.

Unmanned Aerial Vehicles (UAVs) have only recently been applied

in the detection of clandestine graves. With the growing technical

abilities of UAVs, more opportunities are available in methods

for recording data. This opened many doors for detecting hidden

graves because now many different sensing devices can be used

in remote areas that were inaccessible to humans. This study will

compare the use of hyperspectral and RGB images taken by drones

to detect hidden graves. It is aiming to compare how accurately

the graves can be detected post-image processing using the same

technique. The primary motivation is to help future researchers

more easily decide which data collection technique they should use.

The processing technique used on both data sets is a model with

an edge detection algorithm.

My name is Khoa, and I am a senior, double-major in Quantitative Economics and Data Science. My tentative project focuses on the application of Machine Learning to study the physical-chemical properties of different molecule structures, which has been proven useful in many fields like drug discovery, materials science, biology, etc.

Hi everyone, I am Devin. I’m a Data Science major and a senior.

For my project, I am creating a win probability model for the National Hockey League. Hockey has been one of my favorite sports since I was a little kid and applying statistical concepts to one of my favorite sports excites me. Ultimately, I would like to compare the model that I build to other win probabilities for the NHL. The model accuracy would be assessed by how well it can predict which team wins the game.

I am Tra-Vaughn James, a Computer Science major, and Junior:

Today, Bioinformatics is an evolving field, in which computing resources have become more powerful, readily available and workflows have increased in complexity. New workflow management tools (WMT) attempt to develop software that fully harnesses this computational power, creating intuitive implementations utilizing machine learning techniques. This streamlines the design of complex workflows. However, overarching problems still remain that newer workflow management tools do not fully address: they are too specific to particular use cases, and they present a great learning curve for users unfamiliar with computing environments. Many implementations require one to spend copious amounts of time understanding the tool and adjusting already existing frameworks to ones needs, creating frustration and inefficiency. This problem is experienced by both novice and experienced bioinformaticians alike. Using OpenWDL, a Workflow Description Language, as the basis, I seek to develop an open in use workflow management tool coupled with a GUI interface. As OpenWDL is a widely known WMT, its familiarity will aid in my implementations usability. Additionally, the GUI interface will present a more welcoming environment than that of a command line interface in which many WMT’s often employ. To assess the effectiveness of my implementation, I will then assess it to other WMT’s, comparing its usability and openness to other bioinformatic pipeline managers such as SnakeMake and NextFlow.

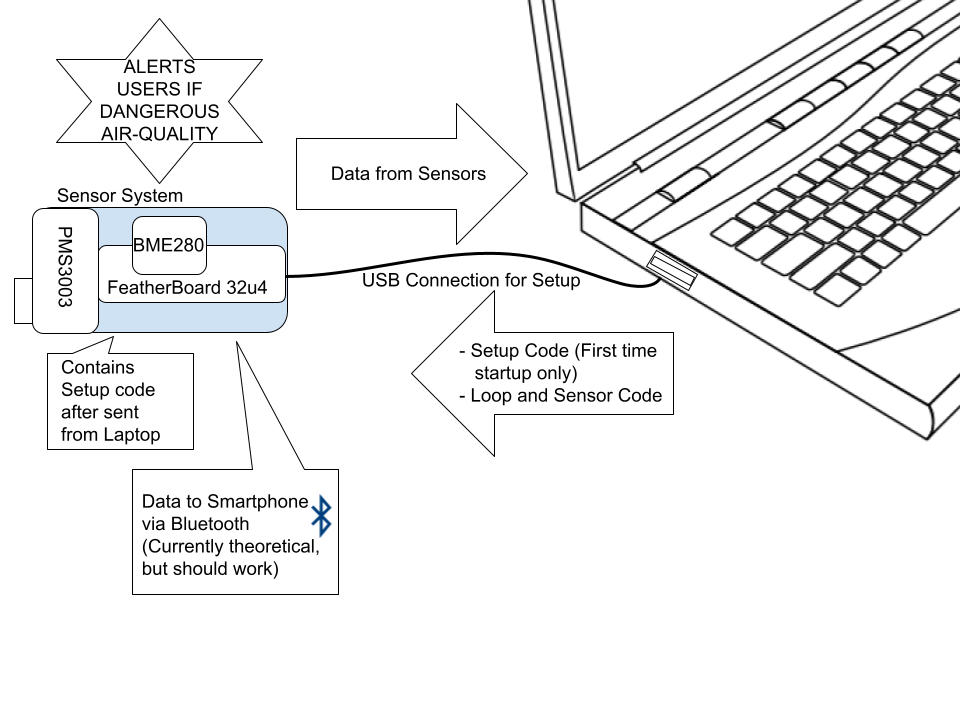

A low-cost portable sensor system allows users to monitor the different components of the air quality around them. There is a need for a sensor system like this because of the millions of deaths and diseases that occur every year due to air pollution worldwide. My planned contribution is for the prototype sensor system I design and build to be as DIY (do it yourself) and low-cost as possible while still being usable in a theoretical online network for large-scale pollution mapping in real time. I will program the sensors together and investigate the calibration of the sensors because they can fall out of calibration after extended periods of time. I will evaluate the results of my experiment of building and using the sensor system by: the robustness of the system indoors and outdoors, analyzing the repeatability of the experiment, accessing how the system could further be improved for ease-of-access to users financially, testing system portability, and the practicality of the theoretical network that could be made with multiple sensor-systems.

https://code.cs.earlham.edu/jccosta181/sensor-system-research

Final Proposal: https://drive.google.com/file/d/1G8MKPq0wwN7Z83wQYncKorOK_4xJpni6/view?usp=sharing

Presentation: https://drive.google.com/file/d/1UC4GmRP-SzGlXY010vyLMKU9AB8n6Y7C/view?usp=sharing

Pitch 1: Website that creates tangible, engaging visualizations of probabilities.

Humans are poor at conceptualizing probability. I notice that one common reason anti-vaxxers use for refusing the vaccine is that they’d rather take their chances with catching covid than get the shot and come down with complications, which is far rarer than the chance of dying from covid. The objective of this project would be to create a website with high user engagement that would inform users of the odds of certain events happening using tangible, engaging visualizations. The user would be able to select from a list of events to compare. Visualizations that represent a dangerous event that is likely to occur will look visually more dangerous than those that are less likely to occur.

I have found some potentially useful datasets to use

Questions

Graphics

Some sources I found that may be useful/interesting:

Pitch 2: Formality indicator for Japanese text

Google translate and Deepl don’t really give users the option to indicate what context a user needs to use Japanese in. One key thing that distinguishes different styles of speech or written communication is the choice in vocabulary. On Jisho, an online Japanese dictionary, some words are marked with what context they are used in. i.e. colloquial, slang, sonkeigo,(Honorific or respectful language). My proposed project would use web scraping from online dictionaries to gather data about which words are used in which context and would tell the user what level of formality the text is in and who it would be appropriate to say/send to.

Ana sent me a list of tools that may be useful. Sudachipy seems promising

Other sources

Pitch 3: Visualization of cause of death

I feel like death statistics are inherently somewhat dehumanizing, and I want to use recent death statistics to create a more human representation. The user would be able to enter certain demographics, such as location, age, sex, etc. This would be pretty similar to pitch one, but I would want to represent each person with something that people would empathize with. Perhaps instead of using the data outright, I would gather patterns from the data to create a fake population. I’m not sure how I might do this

Questions

Problems

I have found several sources for cause of death data on kaggle, but not all are completely recent, which is ideally I am looking for. I did find recent data specifically for Brazil. The CDC has some data as well, I just need to figure out how to get at it.

Pitch #1

The use of computing resources allows the processing of biological data and computational analysis. However in order to conver this data into useful information requires the us of a large number oftools, parameters, and dynamically changing reference data. As a result workflow managers such asSnake and OpenWDL were created to make these workflow scalable, repeatable and shareable. However, many of these workflow managers offer ambiguity toward creating workflows often lacking the specificity many other workflows require. I plan on creating bioinformatics workflow in which can be specified to particular workflows.

Bioshake: A Haskell EDSL for Bioinformatics workflows

Justin Bedő. 2015. Experiences with workflows for automating data-intensive bioinformatics – biology direct. (August 2015). Retrieved January 9, 2022 from https://biologydirect.biomedcentral.com/articles/10.1186/s13062-015-0071-8

Reproducible, scalable, and shareable analysis pipelines with bioinformatics workflow managers

Laura Wratten, Andreas Wilm, and Jonathan Göke. 2021. Reproducible, scalable, and shareable analysis pipelines with bioinformatics workflow managers. (September 2021). Retrieved January 9, 2022 from https://www.nature.com/articles/s41592-021-01254-9

Paper highlights the key features of workflow manager and comapares commonly used approaches for bioinformatics workflows.

A versatile workflow to integrate RNA-seq genomic and transcriptomic data into mechanistic models of signaling pathways

Martín Garrido-Rodriguez et al. 2021. A versatile workflow to integrate RNA-seq genomic and transcriptomic data into mechanistic models of signaling pathways. (February 2021). Retrieved January 9, 2022 from

MIGNON is used for the analysis of RNA-Seq experiments. Moreover, it provides a framework for the integration of transcriptomic and genomic data based on a mechanistic model of signaling pathway activities that allows for a biological interpretation of the results, including profiling of cell activity. Entire pipeline was developed using the Workflow Descriptions Language (OpenWDL). All the steps of the pipeline were wrapped into WDL tasks that were designed to be executed on an independent unit of containerized software by using docker containers, which prevent deployment issues.Paper is an excellent source of seeing how WDL performs as workflow management language and the various problems that can occur from it.

Planning Bioinformatics workflows using an expert system.

Xiaoling Chen and Jeffrey T. Chang. 2017. Planning Bioinformatics workflows using an expert system. (January 2017). Retrieved January 9, 2022 from https://academic.oup.com/bioinformatics/article/33/8/1210/2801462?login=true

ACLIMATISE: Automated Generation of Tool Definitions for bioinformatics workflows.

Michael Milton and Natalie Thorne. 2020. ACLIMATISE: Automated Generation of Tool Definitions for bioinformatics workflows. (December 2020). Retrieved January 9, 2022 from https://academic.oup.com/bioinformatics/article/36/22-23/5556/6039117?login=true

Paper presents aCLImatise which is a utility for automatically generating tool definitions compatible with bioinformatics workflow languages, by parsing command-line help output. This utility can be used withing our workflow to create tool definitions.Workflow definitions must be customized according to the use-case, however tool definitions simply describe a piece of software, and are therefore not coupled to a single workflow or context this aCLImatise will not have a hindrance on workflow creations.

SciPipe: A workflow library for agile development of complex and dynamic bioinformatics pipelines.

Samuel Lampa, Martin Dahlö Jonathan Alvarsson, and Ola Spjuth. 2019. SciPipe: A workflow library for agile development of complex and dynamic bioinformatics pipelines. (April 2019). Retrieved January 9, 2022 from https://academic.oup.com/gigascience/article/8/5/giz044/5480570?login=true

Using rapid prototyping to choose a bioinformatics workflow management system

Michael J. Jackson, Edward Wallace, and Kostas Kavoussanakis. 2020. Using rapid prototyping to choose a bioinformatics Workflow Management System. (January 2020). Retrieved January 9, 2022, from https://www.biorxiv.org/content/10.1101/2020.08.04.236208v1.abstract

Pitch #2

New technologies have been evolving to aid life within the home. Video door bells, cameras and smart devices make many tasks much simpler than they use to be. However, the threat of security and ensuring that those with malicious intent are unable to hack and harm your home network has also increased, a failure in security could expose all of your personal information. As a result of this many organizations provide VPN services that have been developed as a means to protect people from the dangers of malicious hackers and malware. However, these same VPNS come with some faults such as higher cost and limitations as dictated by the provider , and the fact that paid services place you in the hands of the operator and its various cloud/network providers with no certainty that these providers will not snoop around in your data.

A VPN server that a user can host on there local machine solves all of these aforementioned problems with the added benefit of the user being able to securly access and maintain there home network.The server will be held in a virtual machine and will allow the user to be in complete control of it and its functions. This will increase efficiency of the VPN as the user no longer has to go through the network of the provider. My goal is to automate and open-source this process creating an easy launchable VPN server an average user can easily launch and use to maintain access to their home network.While at the same time being capable being edited and changed by the user for more robust security. I seek to compare this to similar paid services identifying which is more secure for the user.

What is a VPN?

Paul Ferguson and Geoff Huston . 1998. What is a VPN. (April 1998). Retrieved January 7, 2022 from https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.169.7689&rep=rep1&type=pdf

Paper defines what a VPN is. Further describes different types of VPN’s such as Network Layer VPN’s how they are constructed and the underlying protocols and techniques used create one. Breaks down the various VPN’s in accordance to the TCP/IP protocol. Describes VPN concepts such as Controlled route leading and Tunnelling. Overall this paper is a good source for understanding the basics of what a VPN is aswell aas the types, and procedures to setup one.

Implementation and analysis ipsec-vpn on cisco asa firewall using gns3 network simulator

Dwi Ely Kurniawan1, Hamdani Arif1, N. Nelmiawati1, Ahmad Hamim Tohari1, and Maidel Fani1. 2019. Implementation and analysis ipsec-vpn on cisco asa firewall using gns3 network simulator. (March 2019). Retrieved January 8, 2022 from https://iopscience.iop.org/article/10.1088/1742-6596/1175/1/012031/meta

This paper provides an example of constructing VPN and testing it using a virtual setting in which is a similar approach in which I am thinking of using. It is built using GNS3 network simulator software and virtual Cisco ASA Firewall. The result shows that VPN network connectivity is strongly influenced by the hardware used as well as depend on Internet bandwidth provided by Internet Service Provider (ISP). In addition to the security testing result shows that IPSec-based VPN can provide security against Man in the Middle (MitM) attacks. However, the VPN still has weaknesses against network attacks such as Denial of Service (DoS) that causes the VPN server can no longer serve VPN client and become crashes.

Enhancing security and privacy in local area network with TORVPN using Raspberry Pi as access point

Mohamad AfiqHakimi Rosli. 2019. Ehancing security and privacy in local area network with TORVPN using Raspberry Pi as access point . (October 2019). Retrieved January 8, 2022 from https://ir.uitm.edu.my/id/eprint/26068/

Provides another method of utilizing VPN servers to protect one’s local network.

Involves the Tor routing technique providing an extra layer of anonymity and encryption.

Although this approach requires the use of Rasberry pie for its implementation it would eliminate the need for installation and configuration of software while also making such services accessible to others.

A Remote Access Security Model based on Vulnerability Management

Samuel Ndichu, Sylvester McOyowo, and Henry Wekesa. 2020. A remote access security model based on … – MECS press. (October 2020). Retrieved January 11, 2022 from https://www.mecs-press.org/ijitcs/ijitcs-v12-n5/IJITCS-V12-N5-3.pdf

Client-Side Vulnerabilities in Commercial VPN’s

Bui Thanh, Rao Siddharth, Antikainen Markku, and Aura Tuomas. 2019. Client-side vulnerabilities in commercial vpns | springerlink. (November 2019). Retrieved January 11, 2022 from https://link.springer.com/chapter/10.1007/978-3-030-35055-0_7

Beyond the VPN: Practical Client Identity in an Internet with Widespread IP Address Sharing

Yu Liu and Craig A. Shue. 2021. Beyond the VPN: Practical client identity in an internet with widespread IP address sharing. (January 2021). Retrieved January 10, 2022 from https://ieeexplore.ieee.org/abstract/document/9314846

Research on network security of VPN technology

Zhiwei Xu and Jie Ni. 2021. Research on network security of VPN Technology. (May 2021). Retrieved January 11, 2022 from https://ieeexplore.ieee.org/abstract/document/9418865

Idea #1

Using machine learning to identify if a webpage is malicious, sometimes websites are blacklisted and that’s how they are identified as malicious but its cumbersome to do that for every website and constant new sites, use ML to identify malicious sites based on keyword density and improve upon existing methods. Other factors that could be used to identify the malicious website are URL length, website age, country of origin. Identifying the most important features to use for ML will be key to the project. A nuance I could add would be to identify the type of attack associated with the URL and rank its severity. Short URLs are a way that malicious attackers attempt to circumvent detection. Being able to expand short URLs in order to extract features could allow for current tools to be more effective.

Idea #2

Calculate expected goals of premier league soccer teams. Expected goals is commonly used as a predictor to help analysts identify skillful players and predict the winning team. There is a mass of datasets to use and techniques that could be analyzed for efficacy and improved upon. A possible nuance I could add is comparing expected goals of a player to their wages or expected goals to the teams’ total wage bill to find efficient teams.

Idea #3

Using machine learning to identify network attacks specifically DOS attacks. Most current methods use huge and cumbersome MIB databases. I would explore more efficient and less time and resource-consuming methods for classifying the data and identifying anomalies within network traffic. Data can be classified by where it comes from, to help determine if it may be malicious. There is less specific research on this topic as most of it is specific to a domain or the data is private.

Idea 1 : Maze Generation

I would like to examine maze generation algorithms for the purpose of generating more challenging domains for search algorithms to solve. Creating domains that challenge existing search algorithms can assist in the development of more robust search algorithms that can avoid certain pitfalls of existing algorithms. Additionally, mazes are widely understood and have efficient state changes, which can allow for more algorithm based examinations in the future. I would like to develop a system for rating the “hardness” of a given maze, as well as creating a maze generation algorithm that can generate mazes that have a higher or lower “hardness” rating.

Idea 2 : Cave Generation Using Cellular Automata

I would like to experiment with using cellular automata to generate cave structures. This has applications in procedural level generation for video games, artistic potential, and depending on the techniques used, it could also be useful in real world geological simulations. There has already been some work done in the area which gives ample room for extension and exploration. Most of the materials seem to be focused on 2D maze generation, so it may be fruitful to focus on generating 3D structures, or extending the existing techniques from 2D CA to 3D.

Idea 3 : Origami Crease Pattern Generation Tool

I would like to build an application that generates an origami crease pattern from a 3D model, with a stretch goal being to implement 3D scanning from a camera. Folding techniques used in origami are seeing more and more uses in engineering contexts. The new Webb telescope for instance used origami for its heat shield and mirrors. Being able to generate crease patterns based on a source model may allow for more widespread use of similar techniques. This project will involve image analysis and potentially machine learning.

Maze generation and solving:

Web application security:

Pitch #1

We all at some point have received that suspicious message stating that we are being watched or an annoying pop up in which insists that our devices are riddled with virus’s. I seek to find out how often and by what measure are people being trully attacked on there smart devices. As many smart devices do not offer robust cyber security systems they are more vulnerable to attack than other devices like computers. This software will provide an insight into the presence of hackers and malware on smart devices gathering data on the types of attacks to be wary of.

Pitch #2

New technologies have been evolving to aid life within the home. Video door bells, cameras and smart devices make many tasks much simpler than they use to be. However, the threat of security and ensuring that those with malicious intent are unable to hack and harm your home network has also increased, a failure in security could expose all of your personal information. As a result of this many organizations provide VPN services that have been developed as a means to protect people from the dangers of malicious hackers and malware. However, these same VPNS come with some faults such as higher cost and limitations as dictated by the provider , and the fact that paid services place you in the hands of the operator and its various cloud/network providers with no certainty that these providers will not snoop around in your data.

A VPN server that a user can host on there local machine solves all of these aforementioned problems with the added benefit of the user being able to securly access and maintain there home network.The server will be held in a virtual machine and will allow the user to be in complete control of it and its functions. This will increase efficiency of the VPN as the user no longer has to go through the network of the provider. My goal is to automate and open-source this process creating an easy launchable VPN server an average user can easily launch and use to maintain access to their home network.While at the same time being capable being edited and changed by the user for more robust security. I seek to compare this to similar paid services identifying which is more secure for the user.

Pitch #3

Many have been contacted by a scam caller and while most have the common sense to recognize the scam being played, thousands of Americans fall victim to such scams and end up paying a huge price for there mistake. While many assume these numbers mainly stem from the elderly, research has shown that people likey to fall for scams are broad in age group with the elderly being scammed for more money and the youth being scammed more frequently. To address this issue I seek to create a real time speech and text recognition answering bot that is capable of answering on phone calls from unknown numbers and through certain verbal ques will be able to deduce weather or not the person on the other end is scammer or not. With this bot I will be able to gather data on the most common types of scams and improve upon existing scam blocker software.

ABSTRACT:

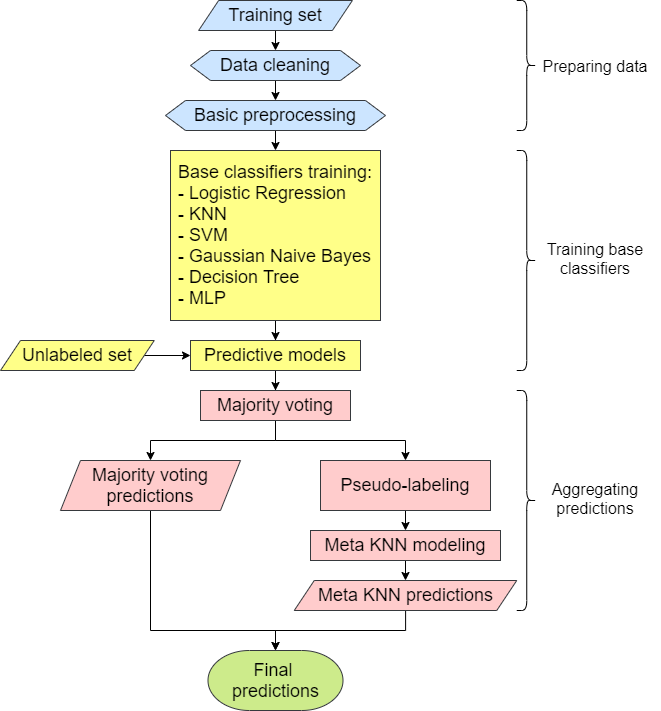

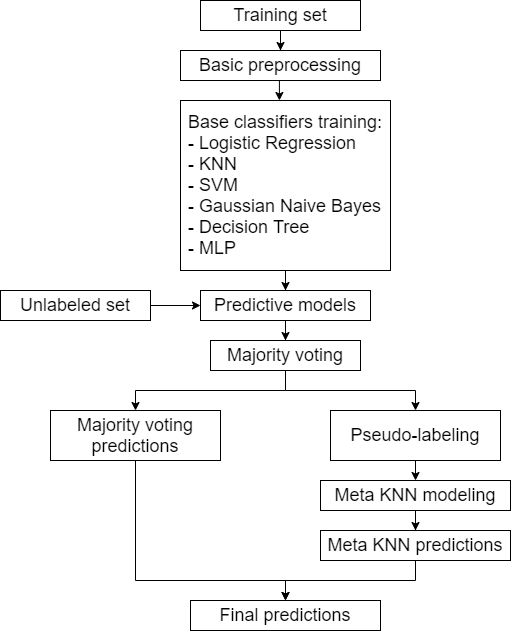

Voting is an important Ensemble Learning technique. However, there has not been much discussion about leveraging the base classifiers’ consensus on unlabeled data to better inform the final prediction. My proposed method identifies the data points where the ensemble reaches consensus and where conflict arises in the unlabeled space. A meta weighted KNN model is trained upon this half-labeled set with the labels of the consensus and the conflict points marked as “Unknown,” which is treated as a new, additional class. The predictions of the meta model are expected to better inform the decision of the ensemble in the case of conflict. This research project aims to implement my proposed method and evaluate it on a range of benchmark datasets.

SOFTWARE ARCHITECTURE DIAGRAM:

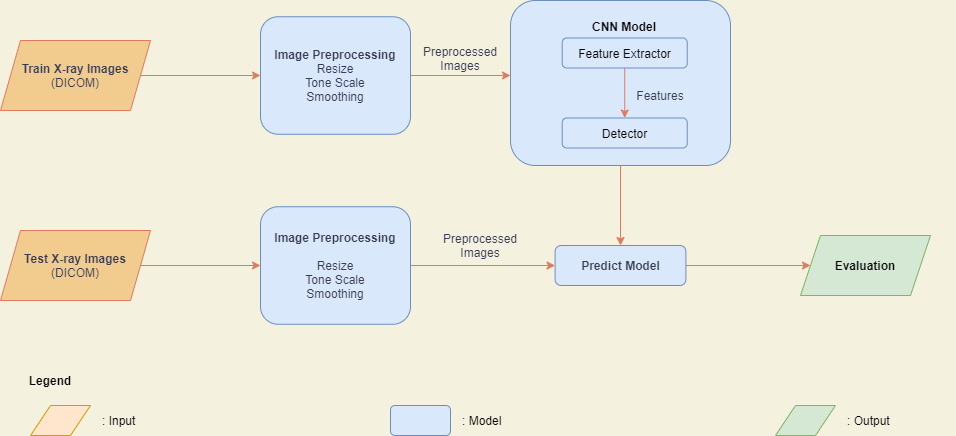

Navigating chest X-rays is an obligatory step to determine lung and heart diseases. Since many people now believe that Chest X-ray radiographs can detect COVID-19, the disease of the decade, the problem of Chest X-ray Abnormalities Detection has gained increasing attention from researchers. Numerous machine learning algorithms have been developed to address this problem to raise reading accuracy, improve efficiency, and save time for both doctors and patients. In this work, I propose a model to determine whether a Chest X-ray image has Infiltration and to detect the abnormalities in that image using YOLOv3. The model will be trained and tested with the VinBigData dataset. Overall, I will use the existing tool, YOLOv3, on a new problem of detecting Infiltration in Chest X-ray radiographs.

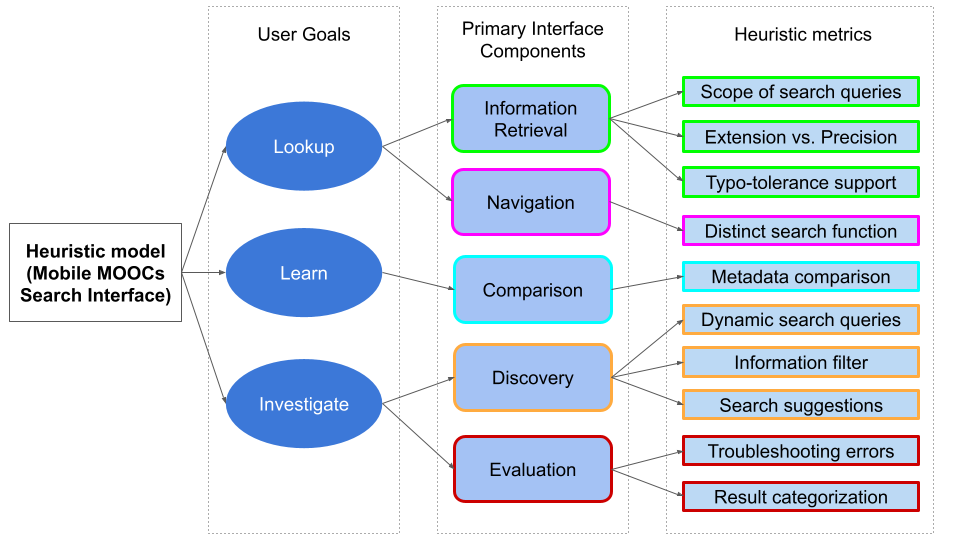

Heuristic evaluation is one of the most popular methods for usability evaluation in Human-Computer Interaction (HCI). However, most heuristic models only provide generic heuristic evaluation for the entire application as a whole, even though different parts of an application might serve users in different contexts, leading HCI practitioners to miss out on context-dependent usability issues. As a prime example, mobile search interfaces in e-learning applications have not received a lot of attention when it comes to usability evaluation. This paper addresses this problem by proposing a more domain-specific and context-dependent heuristic evaluation model for search interfaces in mobile e-learning applications. I will analyze studies on mobile evaluation heuristics, in combination with research in mobile search computing and e-learning heuristics, to generate a heuristic model for mobile e-learning search interfaces.

https://drive.google.com/file/d/17a4p9N_OzE-O7VrwpSl7a9cbAI4Lx_25/view?usp=sharing

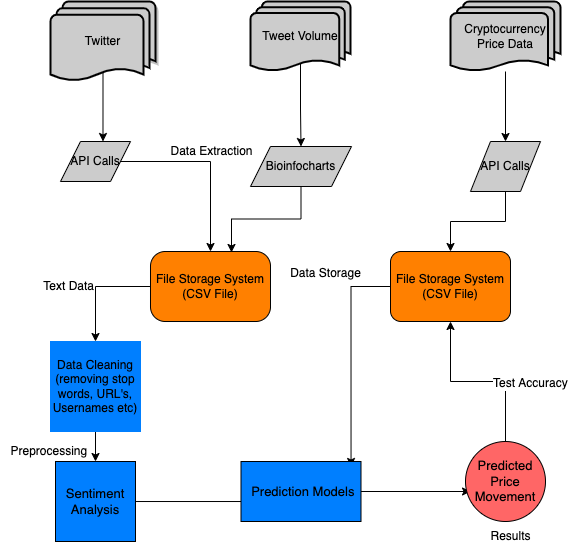

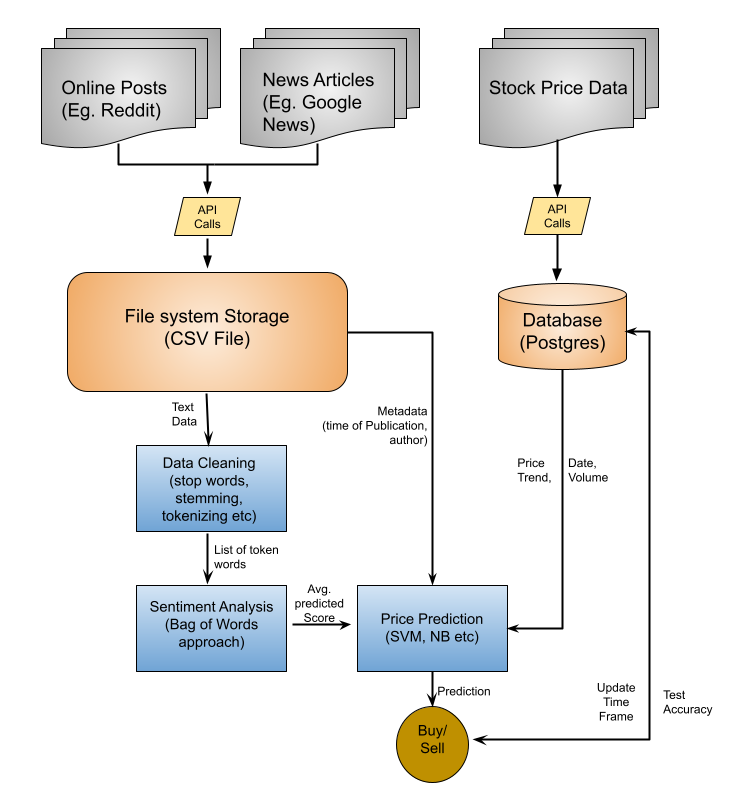

Predicting cryptocurrency price movements is a well-known problem of interest. In this modern age, social media represents the public sentiment about current events. Twitter especially has attracted a lot of attention from researchers who are studying the public sentiments. Recent studies in natural language processing develop automatic techniques in analyzing sentiment in social media information. This research is directed towards predicting volatile price movement of cryptocurrency by analyzing the sentiment on social media and finding the correlation between them. Machine learning algorithms including support vector machine and linear regression will be used to predict the prices. The most efficient combination of machine learning algorithms and the datasets being used will be determined.

Software Architecture Diagram

Link to video tutorial: https://youtu.be/ml4Tc-Xr7bc

Link to senior paper: https://drive.google.com/file/d/1S2TUrBGu8VMmVX1iES8osTWCS6J3PfOG/view?usp=sharing

Pitch 1 – Develop an API for Sensor

I was hoping to work with sensors to develop an interface/app that would be more useful for

individuals’ projects. Say there was this sensor that measured water quality that was inexpensive,

but pretty rudimentary and it doesn’t really have a good API already, I could make an app that

would work with that for individuals who are students or just wanting to do small experiments

with water qualities nearby their house or school. I would work with programming and

interfacing with the hardware sensor. I’m not entirely sure of the dataset I would use or need for

this. I could use one that is already present to work on different graphing techniques in the API.

Pitch 2 – Research into Feasibility and Practicality of Low-Cost Portable Air Quality Sensor and Network with Smartphone Connection

Similar to the sensor pitch I did before, this would be working with air sensors that could be put

into a compact container that would be attached to someone. The sensors would be built into an

Arduino, Charlie said he would show me some sensors and how to use the Arduino sometime

this week when he is back on campus. The air sensors would constantly read for different

dangerous compounds in the air and would notify the user through a smartphone app and track

different amounts in different places. The sensor would not track location, but the app on the

phone would because the sensor would probably be connected to the phone through Bluetooth or

some other possible wireless connection and therefore have to be near the phone to work. This

would be very useful for emergency responders and for maintenance people who work with

boilers and furnaces.

Pitch 3 – Land-Based Oil Spill Modeling